Accounts Reconciliation

Accounts Reconciliation Financial Spreading

Financial Spreading Digital Archive

Digital Archive SchematicIQ

SchematicIQ Loan Ops

Loan Ops Docutwin

Docutwin Contract intelligence

Contract intelligence KYC/KYB

KYC/KYB Form Processing

Form Processing Investment Statements

Investment Statements Enterprise Knowledge

Agent

Enterprise Knowledge

Agent Realtime Intelligence

Realtime Intelligence Customer Support 360

Customer Support 360 Analytica

Analytica CreditIQ

CreditIQ City Intelligence

City Intelligence Smart Utilities

Smart Utilities Connected Worker & Assets

Connected Worker & Assets Drone Based Infra Monitoring

Drone Based Infra Monitoring SceneTrack

SceneTrack

Closing a deal for any business is only half of the battle, the real challenge is to get cash in the bank. In fact, many finance teams admit that they are falling behind in revenue collections. That’s because most invoices get stuck in unorganized collection workflows, and revenue stays trapped on spreadsheets. Eventually, this not only chokes the entire cash flow, but also stalls the overall company’s growth.

But you can quickly fix it through a structured accounts receivable process. Simply put, accounts receivable (AR) is the step-by-step workflow a business uses to invoice customers, track outstanding balances, and collect payments. It creates an operational bridge between making a sale and finally getting paid.

To know more about the AR process, let’s read and learn about the complete AR workflow, common hurdles, KPIs, and best practices to make your collections automated, predictable, and scalable over time.

Key Takeaways

- Accounts receivable workflow acts as the operational bridge that converts closed sales into actual cash flow.

- Effective AR needs a structured eight-step accounts receivable process, starting with the initial credit check and ending with final ledger reconciliation.

- Tracking performance metrics like Days Sales Outstanding (DSO) and Collection Effectiveness Index (CEI) helps finance teams pinpoint AR operational bottlenecks.

- Lately AI-powered platforms like Collatio are taking the centre stage and have become essential for forecasting late payments, automating workflows, and ensuring financial compliance.

What is the Accounts Receivable Process?

The AR process represents the complete lifecycle of a credit sale. It begins the moment a company extends credit to a customer, invoices customers, tracks outstanding balance and ends when the cash successfully hits the corporate bank account.

The AR process defines exactly how fast a business converts its sales into usable working capital. But, most often, the corporate definition of AR is confused with Accounts Payable (AP). Here’s how you can differentiate between them:

- Accounts receivable (AR) is money coming in: This is the cash your customers owe your business for work you have already completed or products you have delivered. If you send an invoice to a client, that unpaid amount is your AR.

- Accounts payable (AP) is money going out: This is the cash your business owes to other companies (like suppliers or contractors) for things you have purchased on credit. If you receive a bill to pay rent or buy server space, that unpaid bill is your AP.

Traditional vs. modern accounts receivable architectures

The existing finance teams usually operate within a traditional or modern accounts receivable approach. The former approach relies heavily on manual effort, isolated spreadsheets, and disconnected software.

Here, the billing data lives in one system; customer communication happens on text/email, and payment records sit in a separate bank portal. This creates a high risk of billing disputes that directly slow down cash flow.

Whereas modern AR architectures replace these isolated steps with a unified, automated, and a cloud-based workflow. This shift has led accounts receivable automation market to expand at a 11.64% annual growth rate.

Further, McKinsey attributes this massive shift directly to AI and advanced analytics, which are actively rewriting the rules of the invoice-to-cash cycle. Here is a direct comparison of how teams manage incoming funds under both models:

| AR Function | Traditional (Manual) Architecture | Modern (Automated) Architecture |

| Invoice Generation | Typed by hand in spreadsheets | Created instantly from sales data |

| Customer Follow-Ups | Manual emails and personal calendar tracking | Scheduled payment reminders based on exact terms |

| System Integration | Disconnected data across multiple software limits | Unified CRM, ERP, and payment gateways |

| Cash Application | Humans check bank portals daily | Automatic data reconciliation of deposits to open invoices |

Core business objectives for an effective accounts receivable management process

A well-managed AR architecture serves several fundamental business goals:

- Accelerates cash flow: A reduction in time between invoice issuance and payment receipt makes sure that the business has the liquidity to operate and scale.

- Minimizes bad debt: Early identification of high-risk customers protects against unpaid invoices and avoids permanent financial losses.

- Improves client relationships: A predictable, error-free invoice experience prevents buyer disputes and keeps customers satisfied.

- Reduces operational costs: Elimination of manual data entry lowers the administrative cost associated with individual invoice workflows.

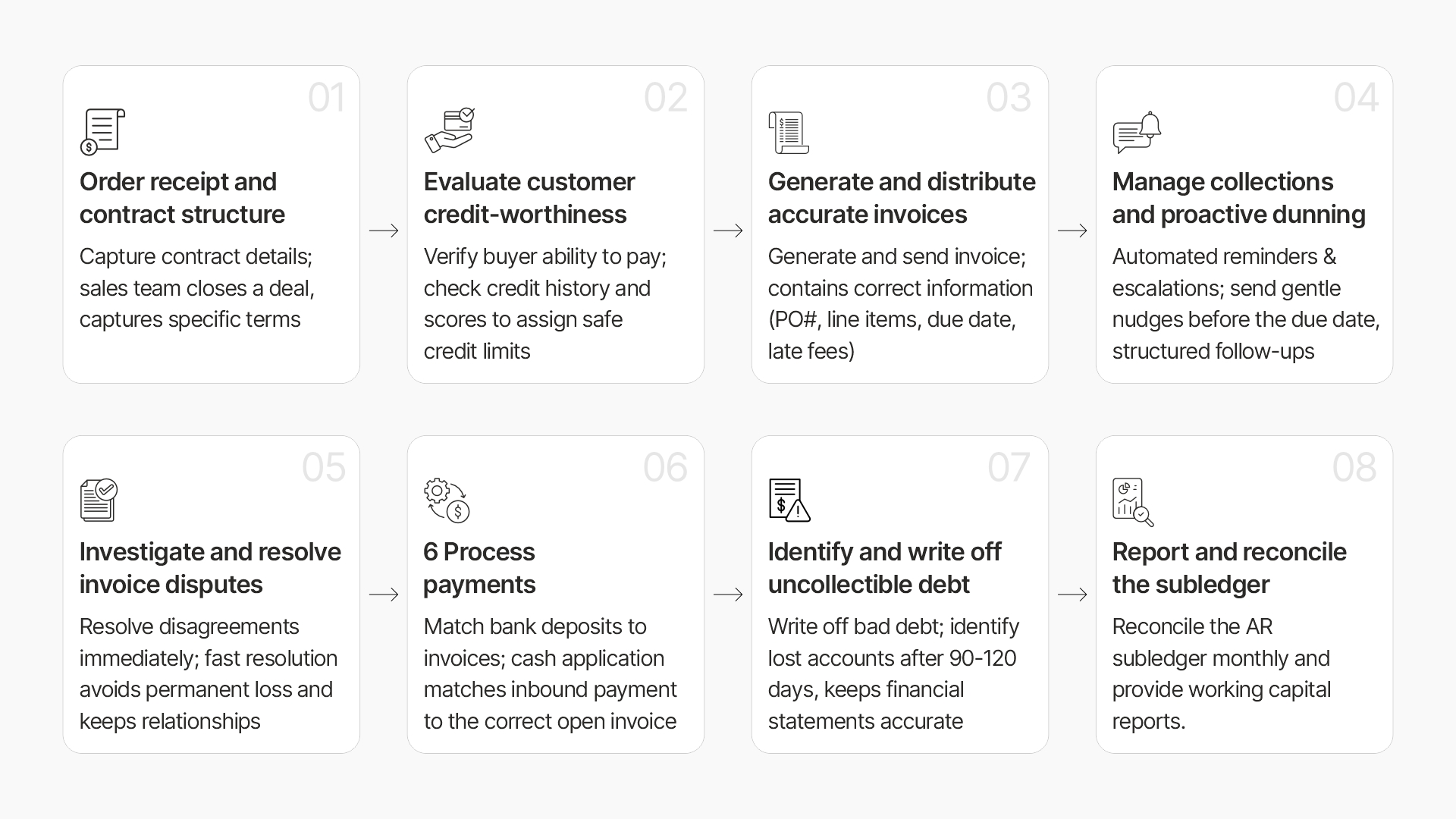

8-step Accounts Receivable Workflow Explained

Every missed detail or communication gap along the cycle creates a hurdle. Here is the chronological end-to-end accounts receivable process to break down how money moves from the initial agreement to your company’s balance sheet. Let’s look at the steps in accounts receivable process:

Step 1: Order receipt and contract structure

The process of accounts receivable begins right when sales teams close a deal. At this stage, they must capture specific contract details like the purchase order (PO) number, the exact contact person, total amount, discount, date, quantity, and other terms & conditions.

Step 2: Evaluate customer creditworthiness

Before you deliver goods or services on credit, you need to verify that the buyer can actually pay. This step involves a check of business credit scores and a review of financial histories to assign a safe credit limit. Omission of this evaluation exposes your business to high-risk clients who might default on their payments later.

Step 3: Generate and distribute accurate invoices

As soon as the finance team identifies the customer and analyzes their credit scores, they must generate an invoice. The invoice must contain correct information, like the PO number, line items, contact details, owed amounts, and the exact due date. If you charge a fee for late payments, you must express this clearly in the document.

Step 4: Manage collections and proactive dunning

Customers rarely pay on the exact day they receive a bill. Therefore, rather than wait until a bill is severely overdue, proactive teams send gentle, automated nudges a few days before the due date. A structured sequence of escalations follows if the deadline passes.

Step 5: Investigate and resolve invoice disputes

Sometimes clients refuse to pay. It could be because they disagree with the charges, hold an undelivered product claim, or spot a calculation error. Therefore, finance teams must investigate these disputes immediately. A fast resolution keeps the customer relationship intact and avoids a permanent loss.

In some cases, customers might just pay the portion of their invoice not in dispute. This adds another layer of complexity for your AR team. You need to confirm why the client made these partial payments and how to record them in the accounting system.

Step 6: Process payments and apply cash

When the customer finally transfers the money, the work is not finished. Cash application is the process of matching the inbound bank deposit to the correct open invoice in your accounting system. If a client pays multiple invoices with one lump sum, identification of the exact bills to mark as paid becomes a tedious manual task without the right software.

Step 7: Identify and write off uncollectible debt

Despite your best efforts, some clients will never pay their invoices due to bankruptcy, billing disputes, or fraud. After a certain period, usually 90 to 120 days past due, finance teams must identify these lost accounts and write them off as bad debt. This keeps the company’s financial statements accurate and realistic.

Step 8: Report and reconcile the subledger

At the end of the month, the finance department must ensure that the accounts receivable subledger perfectly matches the general ledger. Performing regular accounts receivable reconciliation keeps your financial statements accurate and provides leadership with a clear view of the company’s working capital. Hence, you must regularly monitor these KPIs to check on your credit challenges and priorities.

Helpful read: Month-End Reconciliation Process Explained Step by Step

Key Accounts Receivable KPIs and Metrics to Track

Finance leaders rely on these specific performance metrics to measure the speed and efficiency of their collections workflow:

Days sales outstanding (DSO)

It is the average number of days it takes to collect payment after issuing an invoice. If the number is more than 30-45 days (depending upon the industry), then it’s a clear indicator that the overall speed is low, and certain things like invoicing, follow-ups, collection, etc., are slow in the process.

Average days delinquent (ADD)

While DSO measures how many days later a payment was made, in contrast, ADD measures exactly how many days past the agreed due date an invoice remains unpaid. A high ADD clearly indicates a problem in the collection process.

Collection effectiveness index (CEI)

CEI shows the amount of cash you successfully collected against the total amount which was required to collect. A score near 100% proves your follow-up, escalation, or dispute rates, or other procedures have worked.

Accounts receivable turnover ratio

This KPI shows how many times a year your business collects its average AR balance. A high ratio means you convert credit sales into cash rapidly

Invoices per full-time employee

Tracks how many invoices a single full-time employee can process. A low number highlights a heavily manual workflow tracking, which further incurs overall operational cost.

Revenue leakage

This measures the money lost to unbilled services, calculation errors, or missed renewals, showing where earned revenue slips through the cracks.

Bad debt to sales ratio

The percentage of your credit sales that end up uncollectible and permanently written off directly indicates your credit tracking process. It shows how the credit policies are working and whether specific customer segments or payment terms carry higher risk.

Common bottlenecks hampering the accounts receivable process

Even with a defined workflow, finance teams frequently run into operational friction that traps working capital. Here are the primary reasons slowing down your process of accounts receivable:

Manual invoicing and spreadsheet management

Typing data manually introduces errors like wrong pricing or missing PO numbers, which causes instant invoice rejections and costly rework. This manual approach limits your team’s capacity, meaning you have to hire more staff just to keep up as sales grow. It also makes it incredibly difficult to track real-time invoice statuses across the department.

Disconnected financial systems

When your CRM, ERP, and payment gateways operate in isolation, your working force has to spend hours manually matching bank deposits to open invoices. This lack of integration creates a massive reconciliation backlog at the end of every month.

It leaves leadership without a clear, accurate picture of available working capital until the books are finally closed. Fixing this disconnect is exactly why companies are upgrading their technology. In fact, organizations using cloud ERP systems with embedded AI assistants are projected to achieve a 30% faster financial close by 2028.

Internal communication lapses

If sales teams negotiate custom terms but fail to pass that exact data to finance, the resulting invoice will inevitably trigger a dispute. Resolving these internal disconnects wastes valuable time and frustrates the client right at the start of the relationship.

Inconsistent, manual follow-ups

Relying on human memory to send individual collection emails means payment reminders can be skipped. This can further push your DSO higher. It also forces your finance team to adopt inconsistent follow-ups to reach out to late payers. Customers often prioritize paying vendors who have a systematic, predictable follow-up cadence.

Friction in the payment experience

Forcing B2B buyers to rely on legacy payment methods like cash or checks, rather than offering secure, self-service payment portals, directly delays incoming cash. Modern buyers expect a smooth checkout experience where they can view their balance and pay online via credit card or instantly.

Inadequate credit risk assessment

Approving credit terms based on outdated or incomplete financial checks exposes the business to high-risk buyers who are likely to default. Therefore, treating every new client with the exact same terms can hamper your financial health. Plus, failing to continuously monitor credit scores means you might unknowingly extend credit to a company quietly going bankrupt.

Proven Best Practices for Accounts Receivable Management

To fix the operational bottlenecks, your finance team needs a proactive strategy for their end-to-end accounts receivable process. Implementing these targeted practices will help you collect payments faster, reduce administrative rework, and keep your capital intact.

Establish clear credit policies upfront

Before delivering any goods or services, define strict credit rules for your business. You should run proper financial checks and set firm credit limits right at the beginning. This will prevent you from extending risky terms to buyers who are likely to default.

Offer flexible, frictionless payment conditions

If paying a bill requires extra effort, customers will simply delay it. Hence, you must remove technical roadblocks by offering easy-to-use online portals and multiple electronic payment options. This allows clients to settle their balances the exact moment they open the digital invoice.

Standardize your dispute resolution framework

When a client disagrees with a charge, the invoice remains unresolved and unpaid for weeks. Hence, it’s important for you to create a step-by-step procedure for investigating and correcting billing errors immediately.

To make this work, establish cross-departmental Service Level Agreements (SLAs) that require the sales team to confirm original contract terms with finance within 24 hours. Eventually, your business will see fast resolutions, happy customers, and rapid payment collection.

Automate your billing and follow-up communications

Replace manual email tracking with software that automatically generates invoices and triggers scheduled payment reminders. It ensures clients receive consistent, polite nudges right before a due date rather than aggressive demands, without forcing your staff to spend hours chasing down debt.

Review aging reports weekly

You must also track exactly how long the bills are owed to you. Therefore, you must routinely analyze your invoices to identify patterns and escalate your collection efforts on the overdue accounts before they turn into permanent bad debt.

Document clear internal billing procedures

It is important for you to document every step of your invoicing process so anyone in the company can see exactly what details belong on an invoice, when it should be sent, and who should be contacted for clearance.

Future-Proof Your AR with Collatio’s Automation Capabilities

Implementing best practices manually in the accounts receivable process can only take your finance teams so long. To truly eliminate cash flow hurdles, you need a platform like Collatio by ScryAI that handles all while you focus on garnering more clients.

Collatio is an Enterprise AI-powered document processing and digitalization platform. It can work as your accounts receivable automation software and support over 200 document types and classify them for further operations. Let’s see how it can ease the work of the finance team:

- Document digitization & advanced intelligence: Collatio holds the power to digitize Master Service Agreements (MSAs), contracts, quotations, POs, and invoices with 96%+ accuracy. It can even extract precise key terms, dates, and clauses from service contracts to deliver immediate, actionable insights.

- Real-time visibility into balances & reporting: The interactive dashboards provide instant insights into receivables, outstanding balances, cash flow, customer aging, payment status, and trends.

- Identify late payments & optimize credit approvals: Collatio monitors customer accounts automatically based on payment timelines, credits, or negative balances. It flags overdue accounts, highlights delays, and updates outstanding balances dynamically

- Flexible payment options & automated processing: The platform enables businesses to receive payments through multiple channels, including ACH, credit card, check, and international transfers, effectively. It even captures, validates, and applies incoming payments to invoices or grouped customer accounts, ensuring accurate cash allocation and timely ledger updates.

- Exception handling & dispute management: It detects anomalies proactively with rule-based validations that capture missing fields, duplicate invoices, irregular payments, and data inconsistencies. The system automatically flags exceptions and routes them for resolution or manual review, ensuring clear records for compliance and dispute management.

- In-sync, unified AR & AP workflows: Collatio integrates with ERP and accounting systems to maintain consistent data flow between AR & AP workflows. It synchronizes ledger entries, posts approved transactions, and consolidates financial data to support end-to-end visibility.

- Conversational AI insights: Moving forward, your team can make use of Scry AI’s multilingual, conversational AI to receive deep analysis, interactive insights, and on-demand support directly from your data.

Stop letting operational hurdles slow down your cash flow. Book your demo to see how Collatio, our enterprise AI, can secure your data, accelerate your collections, and future-proof your finance team.