Enterprise Knowledge

Agent

Enterprise Knowledge

Agent Realtime Intelligence

Realtime Intelligence Customer Support 360

Customer Support 360 Analytica

Analytica CreditIQ

CreditIQ City Intelligence

City Intelligence Smart Utilities

Smart Utilities Connected Worker & Assets

Connected Worker & Assets Drone Based Infra Monitoring

Drone Based Infra Monitoring SceneTrack

SceneTrack

Dr. Alok Aggarwal

Accounts Reconciliation

Accounts Reconciliation

Financial Spreading

Financial Spreading

Digital Archive

Digital Archive

SchematicIQ

SchematicIQ

Loan Ops

Loan Ops

Docutwin

Docutwin

Contract intelligence

Contract intelligence

KYC/KYB

KYC/KYB

Form Processing

Form Processing

Investment Statements

Investment Statements

Transform Your Workflow with Scry AI Automation

Get StartedThis is an updated report on Knowledge Process Outsourcing with figures that analyse the predictions for the future growth of KPO in India that we made more than three years ago. In this new study, we review the evolution of KPO to date and update our predictions for the industry for the rest of the decade.

During the late 1990s, the success of Information Technology and Business Process Outsourcing to low-wage

countries and the resulting cost savings prompted several multinational companies to experiment with outsourcing

higher-end knowledge-based work. For example:

Although a few companies began providing higher-end, knowledge-based services as early as 1997, this trend did

not gain much momentum until 2003, and it was Evalueserve’s Chief Operating Officer, Ashish Gupta, who coined

the term Knowledge Process Outsourcing (KPO) in an effort to differentiate between his firm’s services and those of the established BPO firms. “KPO” has since come to refer to those outsourcing activities that require significant domain expertise (e.g., market research, business research, investment research, and data mining).

Shortly afterwards, in January 2004, I gave a seminar at Telcordia Laboratories in New Jersey titled, “Moving Up the

Value Chain in Broad Based Outsourcing Services,” wherein I provided Evalueserve’s forecasts regarding the growth

of the KPO industry from 2003-04 to 2010-11. The contents of this talk were later summarized in a July 2004 report,

titled “The Next Big Opportunity – Moving Up the Value Chain – From BPO to KPO” which essentially stated that the

entire KPO sector worldwide would increase from a revenue base of US $1.2 billion in 2003-04 to US $17 billion in

2010-11. Furthermore, within India, this sector would increase from a revenue base of US $1.08 billion in 2003-04 to

US $12 billion in 2010-11, and employ approximately 250,000 professionals in 2010-11.

Since this seminal paper in 2004, the acronym KPO has become part of the lexicon of the outsourcing industry

worldwide. Indeed, more than fifteen independent articles have been written on this topic (including those from

Deloitte Consulting, TPI, and PriceWaterhouseCoopers); at least seven firms providing such services have KPO as

part of their name; there are at least five annual conferences worldwide that are solely about KPO (and some even

have “KPO” as part of their names); about 120 captive units of large multinational companies are providing KPO

services to their offices in North America and Europe; the majority of the mid-sized and large IT and BPO companies

in India have a KPO division; and there are at least 262 “niche” companies in India providing third-party KPO

services.

In this article, we revisit our July 2004 report and analyse how this sector has changed during the last three years

and how it is expected to grow during the next four. We also delve deeper into the sub-sectors within the KPO

industry that are expected to do well (e.g., banking, finance, securities and insurance research; data mining and

analytics; and contract research organisations and biotech services) versus those that are still at a nascent stage

(e.g., legal and paralegal support services; remote logistic services and procurement support services; and network

optimisation and analytics services.)

A business process that is repeatable, scalable and that does not require the physical presence of a worker near the

client can theoretically be outsourced and offshored; this forms the basis of Business Process Outsourcing or BPO. A

Business Process Outsourcing or Offshoring firm’s function can be simply defined as follows: it acquires a process

from the end-client and runs it at its site until the process has reached its logical conclusion, after which it sends the

results – if any – to the client. In contrast, a KPO or Knowledge Process Outsourcing firm functions at a higher level

and can be differentiated from BPO firms in the following ways:

As a final remark, it is worth mentioning that although most Knowledge Process Offshoring services are being

provided from India, countries such as the Philippines, Russia, Ukraine, Poland, Hungary, China and South Africa

are beginning to provide more and more KPO services. Indeed, in the near future, Knowledge Process Outsourcing

and Offshoring is likely to be driven by factors such as breadth and depth of coverage, domain expertise, location

advantage (e.g., near-shoring and language capabilities), sales and marketing capabilities, data compliance with

respect to regulatory standards (especially those defined by the United States, Canada and the European Union) and

the management of business risks. Hence, it is quite likely that companies – both those with their own captives and

those that use third-party vendors – may use a “hub and spoke” model, in which a provider in India constitutes the

“centre” and other units around the world provide appropriate “spokes.”

According to Evalueserve’s research, the revenue earned by the Knowledge Process Offshoring industry worldwide

was approximately US $1.2 billion in 2003-04 and US $4.4 billion in 2006-07; this implies an annual growth rate of 54

percent. Furthermore, the Knowledge Process Offshoring industry employed approximately 34,000 and 106,000

professionals in 2003-04 and 2006-07 respectively. Our forecasts also show that the industry is expected to grow to

US $16.7 billion in revenue in 2010-11 (which would imply an annual growth rate of 39 percent during the next four

years) and to employ approximately 350,000 professionals globally. In contrast, the rest of the Business Process

Offshoring industry worldwide grew from revenue of US $7.7 billion in 2003-04 to US $15.8 billion in 2006-07, which corresponds to an annual growth rate of approximately 27 percent. During the next four years, the BPO industry is

expected to grow annually at 26 percent, thereby earning US $39.8 billion in revenue during 2010-11.

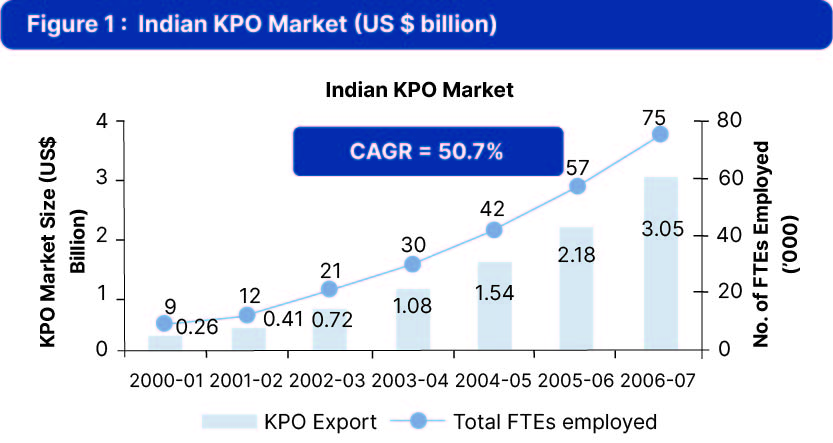

Figure 1 shows the growth of the KPO industry in India from 2000-01 to 2006-07. According to Evalueserve’s

research, although this industry had only 9,000 billable professionals in India that generated total revenue of US

$260 million during 2000-01, this number had already grown to 75,400 by 2006-07 and these billable professionals

generated US $3.05 billion. This implies a cumulative annual growth rate of 51 percent in US Dollar terms and 43

percent with respect to the increase in the number of billable professionals during these six years.2

Interestingly, the growth of the KPO industry

so far seems to be pretty much in line with

Evalueserve’s July 2004 forecasts, where we

estimated that this industry would generate

US $2.9 billion in revenue during 2006-07.

However, we believe that our original

estimate of $11.9 billion being generated by

this industry during 2010-11 may fall short by 6-7 percent, primarily because (a) a few sub-

sectors (e.g., legal, paralegal, intellectual property services, and medical content

creation) have not been growing as rapidly as

expected earlier, and (b) the KPO sector in

India is experiencing substantial employee

turnover, which hurts this sector in particular

because these employees are unable to gain sufficient domain expertise and knowledge before they move on to their

next job.

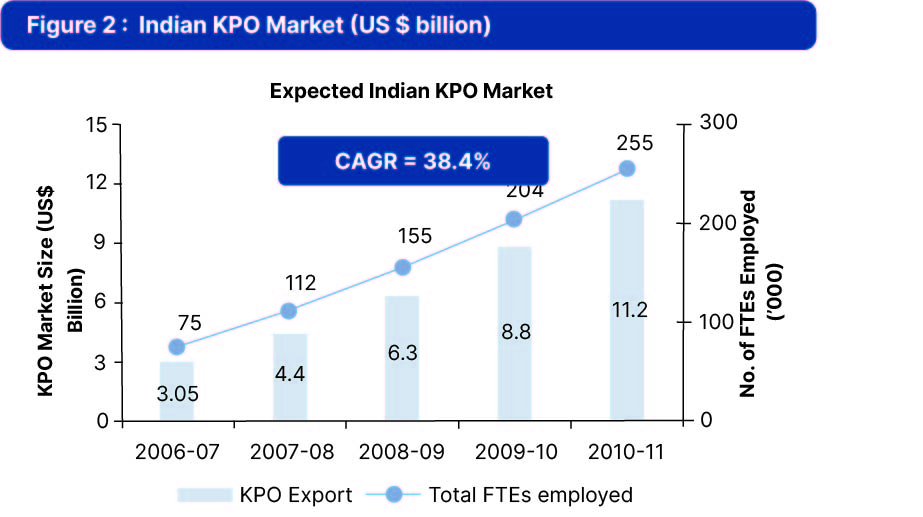

Figure 2 depicts Evalueserve’s current

forecasts with respect to the revenue earned

by this sector during the next four years, as

well as the number of billable professionals it

employs. These forecasts imply a

cumulative annual growth rate of 38 percent

in revenue and 36 percent in the number of

billable professionals (during the next four

years). Clearly, the future is very hard – if

not impossible – to predict and any forecast

comes with some associated assumptions.

Some of the assumptions associated with

the forecasts given in Figure 2 include:

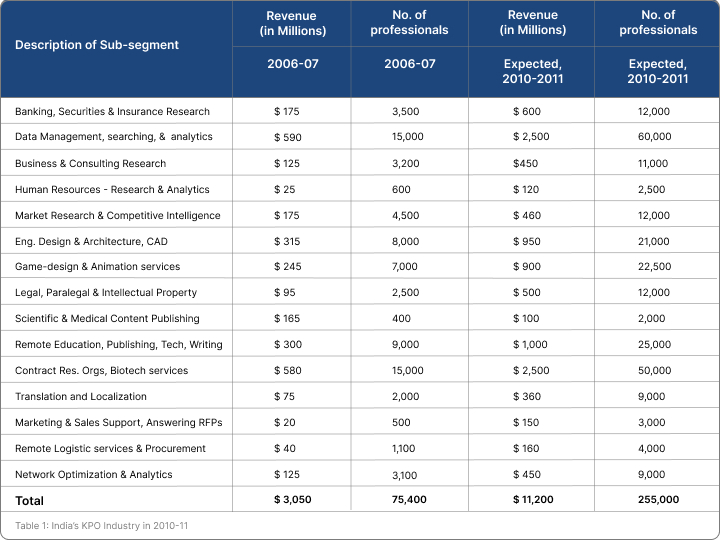

Figure 3 provides estimates for the number of billable professionals likely to be employed in various sub-sectors

within the KPO industry in India during 2010-11 and the revenue generated within these sectors. Of course, the

delineation between some of the sectors is somewhat arbitrary and both the revenue and the number of billable

professionals among them are fungible. Of all the sub-segments of India’s KPO sector alluded to in Figure 3, we

describe three in sections 4.1, 4.2 and 4.3 that seem to be poised for substantial growth and one in section 4.4 that

still seems to be at a nascent stage of development:

There are currently 3,500 billable professionals in this sector in India, of which approximately 1,100 are doing

research related to risk management for credit card and capital leasing companies as well as insurance research.

The remaining 2,400 billable professionals are involved in helping sell-side and buy-side analysts in bulge bracket

banks (e.g., Citigroup, Merrill Lynch, Morgan Stanley, and JP Morgan), mid-tier M&A banks, independent research

providers, hedge funds, mutual funds, pension funds and private equity groups. Given the strong M&A activity that is

ongoing worldwide, the demand for investment research analysts has been growing at a furious pace and clients in

high-wage countries would use an even higher number of high-quality professionals, if low-wage countries like India

could train and provide them.

Given the cost pressures related to research and development of new drugs, biotech and pharmaceutical companies

– both large and small – are outsourcing a lot of clinical research trials to countries in Eastern Europe, India and

China. In fact, according to a recent study by McKinsey and Company, the clinical trial segment in India is expected

to earn US $1.5 billion in revenues by 2010.[Please check changes – I think McKinsey is well-known enough not to

need a description.] Furthermore, our forecasts reveal that the Indian Biotech sector is expected to attain $6.6 billion

in revenue during 2010-11, and about one-fourth of this revenue will come from biotech services’ exports, particularly

in the agricultural biotech and bio-pharmaceutical services areas.

This sector has been growing quite substantially and is likely to grow even faster during the next 3-5 years, especially

because it requires mainly quantitative skills and only limited English speaking and writing skills. Within this sector,

three verticals – banking, finance, securities and insurance; biotech, pharmaceuticals and healthcare; and wireless,

wire-line and cable – are likely to witness massive growth. Indeed, three large data providers in the financial services

industry – Thomson Financial, Reuters and Standards & Poor – put together have approximately 8,000 professionals

working in India in this sub-sector (out of the total of 16,000 professionals mentioned in Figure 3). Collecting and

“scrubbing” data at a fairly low cost and with high quality seems also to be an irresistible proposition for other data

providers.

There are currently more than 60 firms providing legal research, and paralegal and intellectual property-related

services from India; about 45 percent of these are established law firms who practise in India and have now started

providing such additional services. Since the culture in these law firms is substantially different from that of the US, since Indian English is idiomatically different from American and British English, and since lawyers are usually risk-

averse, it is clear that growth in this area will be slow, albeit pronounced (when compared to other sub-sectors within the KPO industry). Also, companies from the Philippines will compete strongly with those from India in providing legal

support and paralegal services to the US, because the Philippines was an American colony until 1946 and its laws

continue to be similar to those of the United States. Nevertheless, even within this sub-sector, some services, such

as those related to intellectual property research, will be offshored more substantially than others, because of the

availability of a large technical talent pool within India.

Blog Written by

CEO, Chief Data Scientist at Scry AI

Author of the book The Fourth Industrial Revolution

and 100 Years of AI (1950-2050)