Enterprise Knowledge

Agent

Enterprise Knowledge

Agent Realtime Intelligence

Realtime Intelligence Customer Support 360

Customer Support 360 Analytica

Analytica CreditIQ

CreditIQ City Intelligence

City Intelligence Smart Utilities

Smart Utilities Connected Worker & Assets

Connected Worker & Assets Drone Based Infra Monitoring

Drone Based Infra Monitoring SceneTrack

SceneTrack

Dr. Alok Aggarwal

Accounts Reconciliation

Accounts Reconciliation

Financial Spreading

Financial Spreading

Digital Archive

Digital Archive

SchematicIQ

SchematicIQ

Loan Ops

Loan Ops

Docutwin

Docutwin

Contract intelligence

Contract intelligence

KYC/KYB

KYC/KYB

Form Processing

Form Processing

Investment Statements

Investment Statements

Transform Your Workflow with Scry AI Automation

Get StartedThe Venture Capital market in India seems to be getting as hot as the country’s famous summers.

However, this potential over-exuberance may lead to some stormy days ahead, based on sobering

research compiled by global research and analytics services firm, Evalueserve.

Evalueserve research shows an interesting phenomenon is beginning to emerge: Over 44 US-based

VC firms are now seeking to invest heavily in start-ups and early-stage companies in India. These

firms have raised, or are in the process of raising, an average of US $100 million each. Indeed, if these

40-plus firms are successful in raising money, they would garner approximately $4.4 billion to be

invested during the next 4 to 5 years. Taking Indian Purchasing Power Parity (PPP) into

consideration, this would be equivalent to $22 billion worth of investment in the US. Since about

$1.75 billion (or approximately 40% of $4.4 billion) has been already raised, even if only $2.2 billion is raised by December 2006, Evalueserve cautions that there will be a glut of VC money for early-

stage investments in India. This will be especially true if the VCs continue to invest only in currently favourite sectors such as IT, BPO, software and hardware products, telecom, and consumer Internet.

Given that a typical start-up in India would require $9 million during the first three years (i.e., $3

million per year) and even assuming that the start-up survives for three years, investing $2.2 billion

during 2007-2010 would imply investing in 150 to 180 start-ups every year during this period, which

simply does not seem practical if the VCs continue to focus only on their current favourite sectors.

In contrast to the emerging trend highlighted above, Indian companies received almost no Private

Equity (PE) or Venture Capital (VC) funding a decade ago. This scenario began to change in the late

1990s with the growth of India’s Information Technology (IT) companies and with the simultaneous

dot-com boom in India. VCs started making large investments in these sectors, however the bust that

followed led to huge losses for the PE and VC community, especially for those who had invested

heavily in start-ups and early stage companies.

After almost three years of downturn in 2001-2003, the PE market began to recover towards the end

of 2004. PE investors began investing in India again, except this time they began investing in other

sectors as well (although the IT and BPO sectors still continued to receive a significant portion of

these investments) and most investments were in late-stage companies. Early-stage investments have

been dwindling or have, at best, remained stagnant right through mid-2006.

Based on Evalueserve’s experience that includes several hundred research engagements focused on

India and the Indian market for our globally dispersed client-base over the last five years, and also

interviews with VCs, Indian entrepreneurs, consultants, and experts within this ecosystem and our

analysis of data from the Indian Venture Capital Association (IVCA) and Venture Intelligence India,

this article examines whether this new, very large total investment can actually be “absorbed” by

start-ups and early-stage companies in India. We will also describe some of the “ground realities” and

highlight a couple of “best practices” that may help VCs to invest more effectively in India.

Note: Most of this article is restricted primarily to early-stage VC investments, i.e.,

investments in a start-up or a small company when the total amount of external money

invested is typically $9 million or less during its entire period of existence. This will be

followed by a separate article, which will focus entirely on Private Equity investments in

India.

1996-1997 – Beginning of PE/VC activity in India: The Indian private equity (PE) and venture

capital (VC) market roughly started in 1996-1997 and it scaled new heights in 2000 primarily because

of the success demonstrated by India in assisting with Y2K related issues as well as the overall boom

in the Information Technology (IT), Telecom and the Internet sectors, which allowed global business

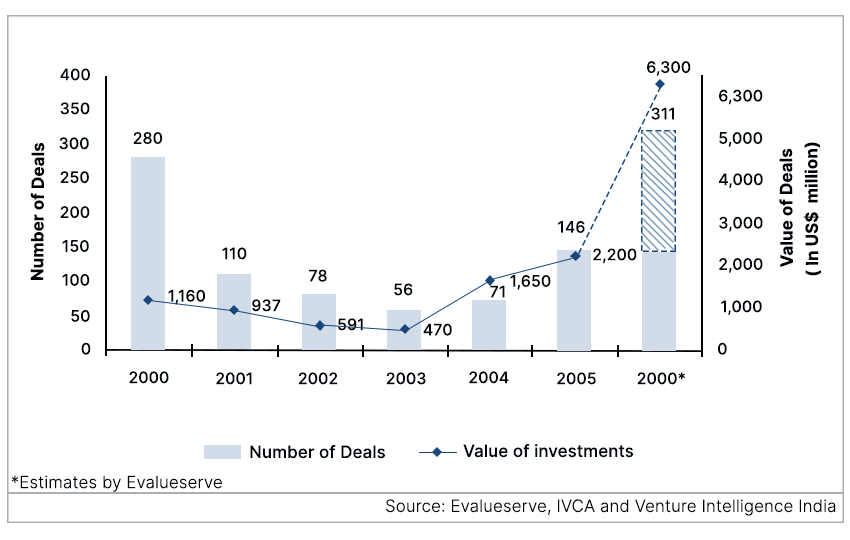

interactions to become much easier. In fact, the total value of such deals done in India in 2000 was

$1.16 billion and the average deal size was approximately US $4.14 million. See Figure 1.

2001-2003 – VC/PE becomes risk averse and activity declines: Not surprisingly, the investing in

India came “crashing down” when NASDAQ lost 60% of its value during the second quarter of 2000

and other public markets (including those in India) also declined substantially. Consequently, during

2001-2003, the VCs and PEs started investing less money and in more mature companies in an effort

to minimize the risks. For example:

2004 onwards – Renewed investor interest and activity: Since India’s economy has been growing at

7%-8% a year, and since some sectors, including the services sector and the high-end manufacturing

sector, have been growing at 12%-14% a year, investors renewed their interest and started investing

again in 2004. As Figure 1 shows, the number of deals and the total dollars invested in India has been

increasing substantially. For example, US $1.65 billion in investments were made in 2004 surpassing

the $1.16 billion in 2000 by almost 42%. These investments reached US $2.2 billion in 2005, and

during the first half of 2006, VCs and PE firms have already invested $3.48 billion (excluding debt

financing). We forecast that the total investment in 2006 is likely to be $6.3 billion, a number that is

more than five times the amount invested in 2000.

Figure 1: Total Number and Value of PE and VC Investments

PE investment expands beyond IT and ITES: A very important feature of the resurgence in the PE

activity in India since 2004 has been that the PEs are no longer focussing only on the IT and the ITES

(IT Enabled Services, commonly known as “Business Process Outsourcing” or BPO) sectors. This is

partly because the growth in the Indian economy is no longer limited to the IT sector but is now

spreading more evenly to sectors such as bio-technology and pharmaceuticals; healthcare and medical

tourism; auto-components; travel and tourism; retail; textiles; real estate and infrastructure;

entertainment and media; and gems and jewellery. Figure 2 shows the division across various sectors

with respect to the number of deals in India in 2000, 2003 and the first half of 2006.

Figure 2: Percentage of the number of deals by PEs in various sectors

| Sectors | 2000 | 2003 | 2006 (Q1&Q2) |

|---|---|---|---|

| IT & ITES | 65.5 | 49.1 | 23.18 |

| Financial Services | 3.13 | 12.3 | 9.7 |

| Manufacturing | 3.0 | 1.8 | 19.3 |

| Medical & Healthcare | 2.0 | 7.0 | 8.3 |

| Others | 25.2 | 29.8 | 37.9 |

| Total | 100.0 | 100.0 | 100.0 |

| Source: Evalueserve, IVCA and Venture Intelligence India | |||

Since the Purchase Power Parity (PPP) in India is approximately a factor of 5 (as in, a factor of 5 is

used to normalize the GDPs of US & India on a PPP basis), our analysis shows that early stage VC

investments in India should include those that are $8 million or less. In fact, we can classify early-

stage investments further into Seed, Series A and Series B investments depending upon their value.

Figure 3: Investment Range of Early-stage VC Deals in India and the US (in US $)

| Year | India | US |

|---|---|---|

| Seed | Up to $900,000 | Up to $2.5 million |

| Series A | $1 million to $3 million | $3 million to $10 million |

| Series B | $3.5 million to $9 million | $11 million to $30 million |

| Source: Evalueserve | ||

Figure 4 given below provides a break-up of the total value of investments into early-stage

investments (primarily by VCs) and late-stage investments and PIPEs (primarily by PEs). Even within

early-stage investments, seed investments declined the most during 2000-2003 and have essentially

remained negligible during 2004-2006.

Figure 4: Value of Deals (in $ millions) Based on the Type of the Investment

| Year | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 (Q1&Q2) |

|---|---|---|---|---|---|---|---|

| Early and Mid Stage VC | 342 | 78 | 81 | 48 | 150 | 103 | 86 |

| Late Stage and PIPEs | 819 | 859 | 510 | 422 | 1,500 | 2,097 | 3,394 |

| Source: Evalueserve, IVCA and Venture Intelligence India | |||||||

Figure 5 shows the break-up of early-stage investments by Seed and Series A and B investments. In a

nuance, perhaps unique to India, after interviewing several entrepreneurs and experts in India, we

believe that since the Indian upper middle class has become quite affluent during the last 7-10 years,

the entrepreneurs are relying more and more on family and friends for seed funding, and since

emerging entrepreneurs come from this upper middle class, the need for seed funding from VCs could

remain low for many years to come!

Figure 5: Number of Early-stage VC Deals

| Year | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 |

|---|---|---|---|---|---|---|

| Seed | 74 | 14 | 7 | 5 | 6 | 5 |

| Series A and B | 68 | 22 | 9 | 8 | 23 | 14 |

| Source: Evalueserve, IVCA and Venture Intelligence India | ||||||

The remaining portion of this article is limited to early-stage VC investments only, i.e.,

investments in a start-up or a small company when the total amount of external money

invested is up to $9 million during its entire period of existence.

Barring occasional forays by VC firms into India in the early to mid-1990s, the first major rush of

VCs to India in recent times was witnessed during the dotcom boom in 1999-2000. However, several

ended up closing shop during 2001-2003 because of the bust that followed. The period 2004-2006 has

seen a resurgence of VC activity. The various VC players operating in India can be broadly classified

as follows:

3.1. Government Funds: Some Indian state government funds are actively investing in India. These

include SIDBI Venture Capital Limited, Gujarat Venture Fund Limited, RVCF, APIDC, Canbank

Venture Capital Fund Limited, IFCI Venture Capital Funds Limited, Rajasthan Asset Management

Co. Private Ltd., KITVEN and Kerala Venture Capital Fund Private Limited. Investments from these

institutions have the advantage of lower ‘cost’ of capital and hence can be more attractive to

entrepreneurs; however, the maximum amount of capital available is typically $500,000.

3.2. Non US-based Funds: These international funds largely invest in early stage and mid stage

companies and include Barings, 2iCapital Private Limited, Aavishkaar India, 3i, (private equity firm

headquartered in Europe), Gaja Capital, Chryscapital Management Companies, HSBC Private Equity

Management (Mauritius) Limited, IL&FS Investments Managers Limited, Information Technology

Venture Enterprises Limited, Indian Direct Equity Advisors Private Limited, Kotak Mahindra Finance

Ltd, Merlion India Fund (Standard Chartered Private Equity), Punjab Venture Capital Limited and

SICOM Capital Management Limited.

3.3. Large Company Funds: For the last 3 to 5 years, many large companies have also been making

early stage and mid-stage VC investments. Such companies are mostly investing in their own

industries and leveraging their expertise with a longer-term view of potential acquisitions. Large

company funds operating in India include those set up by high-tech firms such as Intel, BlueRun

Ventures (owned by Nokia), Motorola, SAP Ventures, Siemens, Acer Technology Ventures, and

Cisco. In addition, several financial companies and a few Indian conglomerates including the

following have small VC funds: Kotak, IDFC, Reliance Capital, JM Financial, Religare (owned by

Ranbaxy), State Bank of India, Banc of America Equity Partners Asia, Unitech (a very large real-

estate developer and manager in India) and Piramal (a well known pharmaceutical company).

3.4. VC Entrants from the US: Evalueserve’s research indicates that several US-based VC funds

have also been investing in the Indian market for the last six years. So far, these funds have been

investing in early and mid-stage technology companies dealing primarily with consumer Internet,

mobile devices, wireless and wire-line, IT services, BPO services, software and hardware products,

electronics and semiconductors. Most of these VC firms are listed in Figure 6.

Figure 6: US-based VC funds investing in India

| Venture Capital Firm | Key Principals | US-India Cross Border & India-based Companies in their Portfolios | |

|---|---|---|---|

| 1 | Westbridge (now a part of Sequioa Capital India) |

Sumir Chadha KP Balaraj Surendra K Jain |

AppLabs, Astra, Brainvisa, Celetron, ICICI OneSource, Indecomm, Induslogic, MarketRx, ReaMatrix |

| Sandeep Singhal | Tarang, Zavata, Dr. Lal PathLabs Royal Orchid Hotels, Bharti TeleSoft Mauj, Nazara, Shaadi, Times Internet Travelguru, Emagia, July Systems, Strand Life Sciences, Zenasis |

||

| 2 | Oak Investment Partners | Ranjan Chak | Talisma, Sutherland |

| 3 | Matrix Partners | Shirish Sathaye Avnish Bajaj Rishi Navani |

Not Available |

| 4 | Sherpalo Ventures and Kleiner Perkins, Caufield and Byers, KPCB) |

Ram Sriram Sandeep Murthy Ajit Nazre |

Cleartrip, Paymate, Naukri.com, 247 Customer |

| 5 | The View Group | Mintoo Bhandari | Integreon, Ingenero, TWS, Tracmail, Peerless India |

| 6 | Bessemer Venture Partners |

Rob Chandra | Shriram EPC, Sarovar Hotels & Resorts Rico Auto Industries, Motilal Oswal Financial Services Ltd |

| 8 | Trident Capital | Venetia Kontogouris | Cognizant, Microland, Outsourced

Partners International |

| 9 | Walden International | In process of hiring more Principals after Dinesh Vaswani left |

Headstrong, e4e, InfoTech, Mindtree Venture InfoTek |

| 10 | New Enterprise Associates (NEA) |

Vinod Dham Vani Kola |

IndusLogic, Sasken |

| 11 | Canaan Partners | Deepak Kamra Alok Mittal |

e4e, Bharat Matrimony |

| 12 | Softbank Asia International |

Ravi Adusumalli | SIFY, Slashsupport, Intelligroup, Investmart, MakeMyTrip |

| 13 | International Finance Corporation |

Paul Asel | Indecomm Global Services |

| 14 | Artiman Ventures | Amit Shah Yatin Mundkur M.J. Aravind Saurabh Srivastava |

BioImagine, Net Devices, Opsource |

| 15 | Columbia Capital | Hemant Kanakia Arun Gupta |

Net Devices, Approva |

| 16 | Gabriel Venture Partners | Navin Chaddha | Allsec, IL&FS Investsmart,

MakeMyTrip, Persistent Systems, Tejas |

| 17 | Norwest Venture Partners | Pramod Haque Vab Goel |

Persistent Systems, Yatra |

| 18 | Austin Ventures | Venu Shamapant Krishna Srinivasan |

Siperia |

| 19 | Sigma Partners | Mark Pine | Emagia Solutions, Kirusa, Zenasis

Technologies, Virtusa |

| 20 | Charles River Ventures | Izhar Armony | July Systems, Virtusa, Net Customer |

| 21 | Financial Technology Ventures |

Eric Byunn | Exlservice |

| 22 | Telesoft Partners | Arjun Gupta Santhil Durairal |

Bombay Cellular |

| 23 | Draper, Fisher, Jurvetson | Raj Atluru | Personiva (f.k.a, Pictureal)

Seventymm |

| 24 | Sierra Ventures | Vispi Daver Tm Guleri |

Everest Software, Astra Business Services, Approva, Razorsight |

| 25 | Battery Ventures | Mark Sherman | Tejas Networks |

3.5. New Groups Raising Money for Investing in India: In addition to the US-based VC groups that

have already invested in cross-border start-ups and in “pure” India-based companies, and excluding

US-based PE firms (e.g., Francisco Partners, Texas Pacific Group, General Atlantic Partners,

Warburg Pincus, Kohlberg Kravis Roberts & Co.) that are likely to make late-stage investments or

PIPEs, our research shows that more than 19 other groups are raising – or have raised – money to

establish funds in India. These groups are primarily US-based VCs, usually with Non-Resident

Indians who are based in the US, who have by and large not made any investments in India. These 19

groups do not include some well known US-based funds (e.g., Greylock and Mayfield) that are in the

process of formulating an “investing strategy for India.” Since some groups have requested anonymity

and confidentiality because they are still in the process of raising money, only 14 out of 19 are

mentioned below:

3.6. Future of Early Stage Investments in India: In summary, our research shows that there are

more than 44 VC groups that have either already raised — or are in the process of raising — between

$40 and $400 million for early-stage investments in Indian companies. If all these groups were

successful in raising money, then jointly they would raise $4.4 billion (i.e., an average size of $100

million per fund) that would need to be invested during the next 4-5 years. Considering the Purchase

Power Parity (PPP) in India is approximately 5, this is equivalent to investing around $22 billion in

the US, which is really large no matter the geography! Since about $1.75 billion (or approximately

40% of $4.4 billion) has already been raised, if we assume just half of this money (i.e., $2.2 billion) is

eventually raised, it would clearly result in a glut of VC money for early-stage and mid-stage

investments in India, especially true if the VCs continue to invest only in currently favourite sectors

such as IT, BPO, software and hardware products, telecom, and consumer Internet.

Given that a typical start-up in India would require $9 million during the first three years (i.e., $3

million per year), and assuming that the start-up in fact survives for three years, investing $2.2 billion

during 2007-2010 would imply investing in 150 to 180 start-ups every year during this period, which would simply not be possible if the VCs continue to focus on their current favourite sectors. This, of

course, would be a marked contrast to the current situation in India (wherein such funding is rather

scarce) and it will also make the market for the ‘right deals’ extremely competitive for these VCs.

Keeping this in view, in the next section, we analyze some of the on-the-ground realities and best

practices for VCs to invest effectively in India.

In many respects, the sophistication and maturity of VC investments in India today are probably at the

same level as in the early 1970s in the US. This section advocates some “best practices” and

highlights some of the key differences between investing in early-stage and mid-stage companies in

the US versus investing in similar companies in India.

4.1. Maniacal focus on early profitability might be counter-productive for a product company: Unlike most start-ups in the US, which are usually product-based and are usually expecting 2-3 stages

of investment, entrepreneurs in India are usually focussed on making their companies profitable as

soon as possible. This mindset might be because Indian entrepreneurs have, to some extent,

traditionally founded services and trading companies. From an Indian entrepreneur’s perspective, the

reasons for making their company profitable quickly include: (a) the scarcity of available venture

capital in India so far, (b) reluctance in giving up too much equity, and (c) since most Indian start-ups

have been in the service sector so far, they require a significantly smaller amount of venture capital.

Of course, the disadvantages of such a maniacal focus on profitability include (a) the possibility that

an Indian start-up may not able to grow very quickly or realize its full potential and (b) the possibility

of an Indian start-up being upstaged by some other firm somewhere else in the world. Hence, the VCs

must play a crucial role in educating Indian entrepreneurs to think differently in the context of

product-based companies compared to how they have traditionally run their companies.

4.2. Need for continued funding but in small amounts: Since the Purchase Power Parity in India is

5, and since many – if not most – Indian start-ups still continue to be created in the services business,

and since the entrepreneurs for even those product-based start-ups wish to achieve profitability

quickly, we believe the VCs should not look at funding Indian companies in distinct stages (i.e., seed

funding, Stage A funding, Stage B funding, mezzanine funding etc). Rather they should provide small

portions of “continuous” funding based on continued attainment of predefined metrics such as

revenues, profits, development expenses, etc. Of course, this would imply that the VC has to be more

involved operationally with the Indian start-up and simply attending a board meeting every two or

three months might not be sufficient. It would also imply that the VC would essentially act as a

“bank” that provides money in exchange for equity, as and when needed.

4.3. Indian entrepreneurs lack marketing, sales and business development expertise: During our

interviews and research, we found Indian entrepreneurs to be quite adept technically and definitely at

par with similar entrepreneurs in developed countries. However, we also found the entrepreneurs in

India generally lacked expertise in marketing, sales and business development areas, especially when

compared to their counterparts in the US. Furthermore, since India had socialistic economic policies

during 1947-1992, there is a lack of good talent in marketing and sales professionals who can thrive in

an extremely competitive environment. Hence, finding the appropriate marketing, sales and business

development people is one area where Indian start-ups need help. This problem is further exacerbated

because the Indian economy has been growing at 8% and most start-ups have to compete for talent not

only with other companies who are exporting similar or dissimilar products and services but also with

many Indian domestic companies. In fact, finding and retaining the ‘right talent’ has become an issue

not only in marketing, sales and business development but also in research, technical and advanced

development areas. Finally, if the eventual market were a developed country, then such expertise can

be potentially found in that country. However, if the market for the corresponding product or service

is India, China or some other developing nation, then finding such people can be a Herculean task!

4.4. Indian entrepreneurs are hesitant to give up control: Indian entrepreneurs are usually hesitant about giving up control. In fact, most of the entrepreneurs in India currently receive their initial 8 funding from family and friends, and even if they do not do so, the Indian social system is such that

relatives and friends still end up being a major influence. Also, since the Bombay Stock Exchange

(BSE) has been growing quite rapidly (in spite of the recent 20% drop) and a company with $20

million in annual revenue can be easily listed on it, many Indian entrepreneurs would rather list their

companies on BSE than give up a substantial share to the VCs. Consequently, the VCs will have to

provide a very clear value proposition to the start-ups and cannot simply state that they bring value to

the table just because they are well connected, etc. In fact, we believe that in some cases the VCs may

even have to go to the extreme of closing contracts and bringing in the revenue on behalf of a start-up

rather than simply “opening doors” by providing the contacts in their “Rolodex.”

4.5. Lack of financial transparency and other processes: Again, partly because the Indian economy

was a “socialistic and closed” economy and partly because Indian entrepreneurs are not as proficient

at business development as their counterparts in the US, Indian start-ups lack financial transparency

and often have limited experience in implementing effective financial processes. This usually makes

the task of the VC much more difficult not only during the due-diligence phase, but also in helping the

start-up grow rapidly. Consequently, we believe that immediately after making its investment, the VC

may have to “roll up the sleeves” and help the entrepreneurs in “process-izing” the company. We also

believe that simply directing the Indian entrepreneurs to implement processes during monthly or

quarterly board meetings may prove to be futile because many entrepreneurs might not know how to

execute on these instructions.

4.6. Investment thesis and the current model is un-sustainable: One of the most worrisome aspects

of the VCs’ new-found zeal to invest in India is that most VCs want to continue to invest in Indian

start-ups in areas they are most familiar with, i.e., in IT, telecom and Internet products and services.

So, it is not surprising that eight consumer-travel Internet websites have already been funded in India,

and given that this sector only accounted for approximately $152 million worth of booking

transactions in 2005, and given that this number is likely to grow to only to $1.2 billion by 2010, the

actual revenue and profits earned by this sector even in 2010 are likely to be $75 million and $9

million respectively, which is miniscule by any standards! Similarly, if we study the cross-border and

“pure” India-based companies listed in Section 2.4, more than 90% are in the IT, ITES and BPO,

Telecom, and Consumer Internet.

So, going forward, the VCs may want to investigate the following rapidly emerging sectors for

potential investment: auto-components, travel and tourism, domestic healthcare and medical tourism,

retail, textiles, biotechnology, pharmaceuticals, real estate and infrastructure, entertainment and

media, gems and jewellery, and of course, the traditional sectors that include telecom, IT, and

Business Process Outsourcing services. An overview of these sectors has been provided in a separate

research paper from Evalueserve.

Finally, it is interesting to note that in this regard, several VC firms (e.g., ChrysCapital, Westbridge –

now a part of Sequoia Capital, India) are beginning to follow a well-rounded and diversified strategy,

but so far most of it is limited to late stage investments and PIPEs. For example, during the last 2-3

years, Bessemer has invested in the following companies:

4.7. Lack of VCs who have cross-border experience: The other really worrisome aspect is that many

US-based VCs believe they can help the growth of Indian start-ups, and provide good returns to their

own shareholders by:

4.8. Well-known US VCs may not have the same brand recognition in India yet: Since venture

capital investing in India is a relatively recent phenomenon, VCs who may be well known in the US

may not yet be able to take their brand recognition in India for granted. In fact, we believe that

successful Indian entrepreneurs and VCs who have lived in the US and have at least ten years of

experience in running their own companies, or have been actively involved in helping others and can

get down in the “trenches” with the Indian entrepreneurs are more likely to succeed and build a brand-

name for themselves and their groups. Of course, on the other hand, since most – if not all – of these

groups are raising the money in the US, brand name VCs in the US will definitely be able to raise this

money much more efficiently and effectively than those groups that are not known in the US. Again,

the implication for the VC firm is that it will have to articulate a very clear value proposition.

Blog Written by

CEO, Chief Data Scientist at Scry AI

Author of the book The Fourth Industrial Revolution

and 100 Years of AI (1950-2050)